In 2015, the consensus view in fintech circles was that traditional banks were about to be eaten alive. The challengers were coming — nimble, digital-native, unburdened by legacy infrastructure and branch networks that cost more to maintain than they generated in foot traffic. The obituaries were being drafted.

A decade later, JPMorgan Chase processed more transactions in 2023 than it did in 2015. The major European banks are still standing. But something fundamental did change — not in who owns the financial system, but in where it lives.

Finance moved from buildings and branches into the background of everything else. The bank didn't die. It became infrastructure. And infrastructure, as anyone who has tried to compete with it knows, is extraordinarily hard to dislodge.

The fintech companies that built durable businesses are not the ones that tried to replace banks. They are the ones that found a specific failure mode — a customer segment being underserved, a process taking twenty days that could take twenty seconds, a pricing structure that made no sense for a particular use case — and fixed exactly that, at scale, without needing to rebuild everything around it.

The ones that struggled discovered, at considerable expense, that the hard parts of banking — credit risk, regulatory compliance, fraud prevention, liquidity management — are hard for structural reasons that a better mobile app does not resolve.

Where the Real Technical Work Is Happening

The embedded finance shift nobody fully priced in

The most consequential shift in financial services over the past five years is not a product or a company. It is a structural change in where financial services happen.

They increasingly happen inside non-financial products — e-commerce platforms, logistics software, HR systems, healthcare applications, retail checkout flows — delivered through APIs by infrastructure providers that most consumers will never interact with directly.

The BNPL product embedded in a checkout flow. The instant payment capability built into a gig economy platform. The small business lending decision made at the point of invoice, inside the accounting software the business already uses. In each case, a financial service was delivered and the incumbent bank was either not present or not visible.

This is the embedded finance stack — and it is where the genuinely interesting engineering and quant work is being done right now.

The infrastructure layer is where durable value accumulates

The companies that built the rails — payment processing networks, banking-as-a-service platforms, KYC and fraud infrastructure, lending decisioning engines, real-time risk systems — are accumulating network effects and switching costs that are structurally similar to the advantages incumbent banks built over the previous century.

They are becoming the new pipes. And pipes, once embedded into operational workflows at scale, are extraordinarily sticky.

The consumer-facing layer — the app, the brand, the UX — is where competition is intense, margins are thin, and customer acquisition costs have made many business models that looked compelling in 2019 look considerably less so in 2024. The infrastructure layer is where the technical problems are genuinely hard and the business models have real structural defensibility.

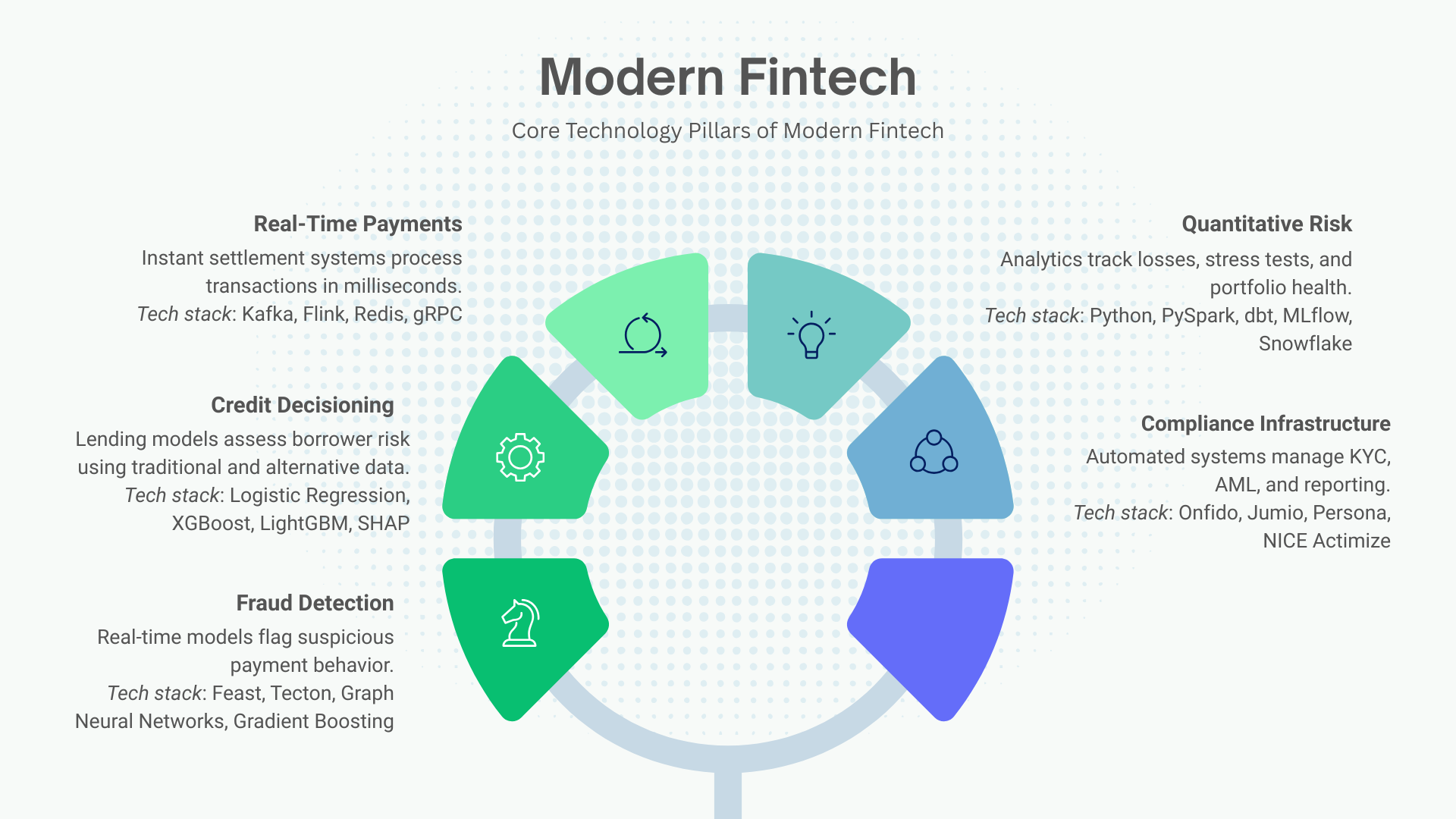

The Tech Stack That Actually Matters in 2024–25

Payments and real-time infrastructure

Modern payments infrastructure has moved decisively toward real-time. In the US, the FedNow Service (launched 2023) and RTP network (The Clearing House) are the rails for instant payment settlement. In Europe, SEPA Instant Credit Transfer and the forthcoming ISO 20022 migration are reshaping how payment messages are structured and routed globally.

The engineering stack underneath real-time payments is demanding: Apache Kafka for event streaming at scale, Apache Flink for stateful stream processing, Redis for low-latency state management, and gRPC for high-throughput inter-service communication. Companies like Stripe, Adyen, and Marqeta have published engineering blogs detailing their approaches to sub-100ms payment authorization at scale — these are some of the best technical writing available on production financial systems engineering.

On the infrastructure-as-a-service side, Plaid (data aggregation), Galileo (card issuing), Synapse (banking-as-a-service, now cautionary tale as well as case study), and Unit represent the API layer that allows non-banks to embed financial products. Understanding how these platforms expose financial primitives through APIs is as important as understanding the underlying ledger mechanics.

Credit decisioning and alternative data

Credit decisioning is the most intellectually honest test of a fintech's actual capabilities. It requires real data, real statistical rigor, real consequences for errors, and real accountability to regulators watching for the kinds of shortcuts that look like innovation from the inside and look like discrimination from the outside.

The modern credit decisioning stack has three distinct layers.

Feature engineering from alternative data is where the differentiation starts. Traditional credit bureaus — Experian, Equifax, TransUnion — provide the baseline. The interesting work is in augmenting this with cash flow data (bank transaction history via open banking APIs), rental payment history, utility payments, employment verification through payroll data providers like Argyle and Pinwheel, and for certain markets, mobile data signals and behavioral biometrics. The Consumer Financial Protection Bureau's 2023 open banking rulemaking under Section 1033 is accelerating the availability of permissioned financial data in the US, with significant implications for credit feature engineering.

Model architecture in production credit decisioning is less exotic than conference talks suggest. Logistic regression remains the most deployed model in regulated credit decisions because of its explainability properties — regulators require that adverse action notices explain why a credit decision was made, and a gradient boosting model does not make this easy. XGBoost and LightGBM are standard for risk ranking where full adverse action explainability is less critical. SHAP values (SHapley Additive exPlanations) have become the near-universal approach for post-hoc model explainability in credit, allowing gradient boosting models to generate feature-level explanations that satisfy regulatory requirements.

The emerging frontier is Graph Neural Networks for fraud and credit risk, exploiting the relational structure of financial networks — shared devices, addresses, phone numbers, and payment relationships — to identify organized fraud rings and synthetic identity fraud that are invisible to models treating each applicant in isolation. PyTorch Geometric and DGL (Deep Graph Library) are the standard frameworks.

Model monitoring and fairness infrastructure is the component most often missing in early-stage fintechs and most often responsible for regulatory difficulties later. Fair lending law in the US (Equal Credit Opportunity Act, Fair Housing Act) prohibits credit decisions that have a disparate impact on protected classes even without discriminatory intent. Adverse impact ratio analysis, marginal effect testing, and increasingly counterfactual fairness methods are required components of a defensible credit model governance framework. WhyLabs, Arize AI, and Fiddler AI are the leading model monitoring platforms with financial services-specific capabilities.

Fraud detection and financial crime

Real-time fraud detection is one of the most technically demanding problems in applied machine learning. The challenge is simultaneously statistical — extreme class imbalance, adversarial distribution shift as fraudsters adapt to detection — and operational — decisions must be made in milliseconds on transaction streams processing hundreds of thousands of events per second.

The standard production approach combines rule-based systems (fast, interpretable, easy to update for known fraud patterns), gradient boosting models (strong performance on tabular transaction features), and increasingly Graph Neural Networks (for network-level fraud pattern detection). Feature stores — Feast, Tecton, Hopsworks — have become critical infrastructure for serving low-latency features to real-time scoring models without recomputing them at inference time.

For anti-money laundering (AML) and transaction monitoring, the regulatory requirements and the machine learning approaches are converging. Network analysis for transaction pattern detection, sequence models for temporal pattern recognition, and large language models for suspicious activity report (SAR) narrative generation are all in production at major financial institutions. NICE Actimize, Oracle Financial Services, and SAS AML are the dominant vendor platforms, but in-house builds at tier-one banks and sophisticated fintechs are increasingly common.

Quantitative risk and real-time decisioning infrastructure

The quantitative risk function at a mid-size lending platform or payments company is doing work technically comparable to quantitative finance at a major bank — with the added complexity of operating in real time on streaming data rather than on daily batch runs.

Market risk in fintech context means largely credit market risk — the risk that the credit quality of a lending book deteriorates. Credit Value at Risk (CVaR) models, stress testing frameworks, and CECL (Current Expected Credit Loss) accounting standards, which require forward-looking lifetime loss estimates on loan portfolios, are the quantitative frameworks that matter.

The data infrastructure supporting these functions has standardized around a recognizable stack: Python (pandas, NumPy, SciPy, statsmodels) for analytical work, PySpark or Dask for distributed computation on large loan portfolios, dbt for data transformation and lineage, Great Expectations or Soda for data quality validation, and MLflow or Weights & Biases for experiment tracking and model registry management. SQL fluency — specifically on analytical databases like Snowflake, BigQuery, or DuckDB — remains the highest-leverage single skill for anyone doing quantitative work in financial services.

Regulatory technology and compliance infrastructure

Regulatory compliance is not a moat in the traditional sense because it is not exclusive. What regulation creates is a shared burden — a minimum cost of operating that disproportionately disadvantages entrants with thin capital and short runways.

The fintech companies navigating the current environment most successfully treated regulatory preparation as a product investment rather than a compliance cost. They built systems that generate audit trails by default, produce regulatory reports as a byproduct of normal operations, and adapt to new requirements without significant re-engineering.

The regtech stack is less glamorous and more durable than most fintech stacks. Know Your Customer (KYC) infrastructure — Onfido, Jumio, Persona — handles identity verification at onboarding. Know Your Business (KYB) for commercial clients is a harder problem, with Middesk and Beneficial Ownership data from FinCEN's new registry being the current state of the art in the US. Transaction monitoring platforms, regulatory reporting engines for Basel III/IV compliance, and model risk management frameworks compliant with SR 11-7 (the Federal Reserve's supervisory guidance on model risk) are the components of a serious compliance infrastructure.

Where the Hard Problems Are Concentrated Right Now

Credit infrastructure for underserved markets

Roughly 26 million Americans are "credit invisible" — no credit file at the major bureaus — and another 19 million are "unscorable" with existing models. Globally, the numbers are vastly larger. The technical challenge of building credit models that work for thin-file and no-file consumers using alternative data is a genuinely hard statistical problem with real economic and social stakes.

Cash flow underwriting — using bank transaction data to assess creditworthiness directly from income and spending patterns rather than from bureau scores — is the most credible technical approach currently in production. Nova Credit (for immigrants with international credit histories), Petal (cash flow underwriting for no-file consumers), and the VantageScore 4.0 model (which incorporates rental and utility payment data) represent different approaches to the same underlying problem.

Real-time risk for embedded finance

As financial services move into non-financial contexts — lending at the point of sale, insurance at the point of need, payments at the point of invoice — the risk models that underlie these decisions need to operate in real time, in contexts where the traditional signals (bureau data, application information) may be limited or unavailable, and where the relationship between the financial infrastructure provider and the end user is mediated by a platform that has its own data and its own incentives.

The risk management framework for embedded finance is still being built. The companies getting there first are building significant competitive advantages.

Compliance infrastructure for the AI Act and open banking

The EU AI Act's high-risk classification for AI systems used in credit scoring has real implications for model documentation, testing, and human oversight requirements that are still being operationalized. The US CFPB's Section 1033 open banking rulemaking, finalized in 2024, creates new data access rights and new data security obligations that will require significant infrastructure investment. These are not abstract regulatory developments. They are near-term engineering requirements.

Building a Durable Career in Fintech Quant

The profile that actually gets hired

The candidates building the most durable careers in fintech are not the ones who joined the most hyped consumer app at the peak of its valuation. They are the ones who found the hard problem — the credit risk model, the fraud detection system, the payments reconciliation infrastructure, the regulatory reporting engine — and got genuinely good at it.

The hybrid profile that is in acute demand: strong Python and SQL, real understanding of statistical modeling for financial applications (not just ML benchmarking), fluency with at least one cloud data platform (Snowflake, BigQuery, Databricks), practical knowledge of a streaming framework (Kafka, Flink), and enough regulatory literacy to understand why a model that works technically might not be deployable.

The learning path worth following

Foundations: Introduction to Statistical Learning (James et al.) for the statistical grounding. Andrej Karpathy's neural network course for deep learning fundamentals. The fastai practical deep learning course for applied ML. These are not fintech-specific — they are the technical foundations that translate into fintech contexts.

Fintech-specific: The Bank for International Settlements publishes working papers on fintech credit, payments, and crypto that are the highest-quality research available on structural questions. The CFPB's technical reports on fair lending and credit scoring are essential for anyone doing credit work in the US. Stripe, Adyen, and Wise publish detailed engineering blogs on their production systems that are worth reading as primary sources.

Datasets to work with: Lending Club loan data (historical, available on Kaggle) for credit modeling. IEEE-CIS Fraud Detection (Kaggle competition dataset) for fraud modeling. FRED (Federal Reserve Economic Data) for macroeconomic features. The Home Mortgage Disclosure Act (HMDA) dataset for fair lending analysis.

Certifications that carry weight: FRM (Financial Risk Manager, GARP) for risk-focused roles. CFA for investment and wealth management adjacent roles. For the technically oriented, AWS/GCP/Azure cloud certifications signal production readiness in ways that are legible to hiring managers at infrastructure-focused fintechs.

Communities: Risk.net for quantitative risk. Quant Finance Stack Exchange for technical questions. MLOps Community for production ML deployment. The GARP and PRMIA networks for risk management practitioners.

Assessment

The fintech revolution didn't kill the bank. It made finance invisible, ubiquitous, and structurally more complex than it has ever been. The companies that thrived are the ones that built the infrastructure underneath the consumer interface — the decisioning engines, the fraud systems, the compliance infrastructure, the data platforms — and got very good at making them work at scale under regulatory scrutiny.

The people who will define the next decade of this industry are not the ones who understand the consumer interface sitting on top of the financial system. They are the ones who understand the infrastructure, the risk, the regulation, and the data underneath it — and who have the technical depth to build systems that work in production, not just in demos.

That combination — quantitative rigor, systems thinking, regulatory literacy, and production engineering discipline — is rarer than the fintech hiring cycle has historically appreciated. It is becoming less rare as the industry matures. The window to build it, and to be genuinely early to the infrastructure problems that the next cycle will be built on, is shorter than it looks.

SB Analysis — This piece draws on SB's editorial research into fintech infrastructure and quantitative finance, including BIS working papers, CFPB regulatory documentation, published engineering research from major payments and lending platforms, and practitioner conversations conducted across the US and European markets in 2023–24. These are our assessments, not original empirical claims.

Explore more writing on topics that matter.